Mathew事案

目次

Mathew v. Canada, [2005] 2 S.C.R. 643, 2005 SCC 55

概要

パートナーシップの構成員であった納税者が、不動産の含み損を損益通算することで租税回避を行った事案。課税庁は所得税法の一般的租税回避防止規定(GAAR)を適用して、当該所得控除を否認した。

相関図

GAAR適用の3段階 Canada Trustcoを引用 「一連の取引」を重視

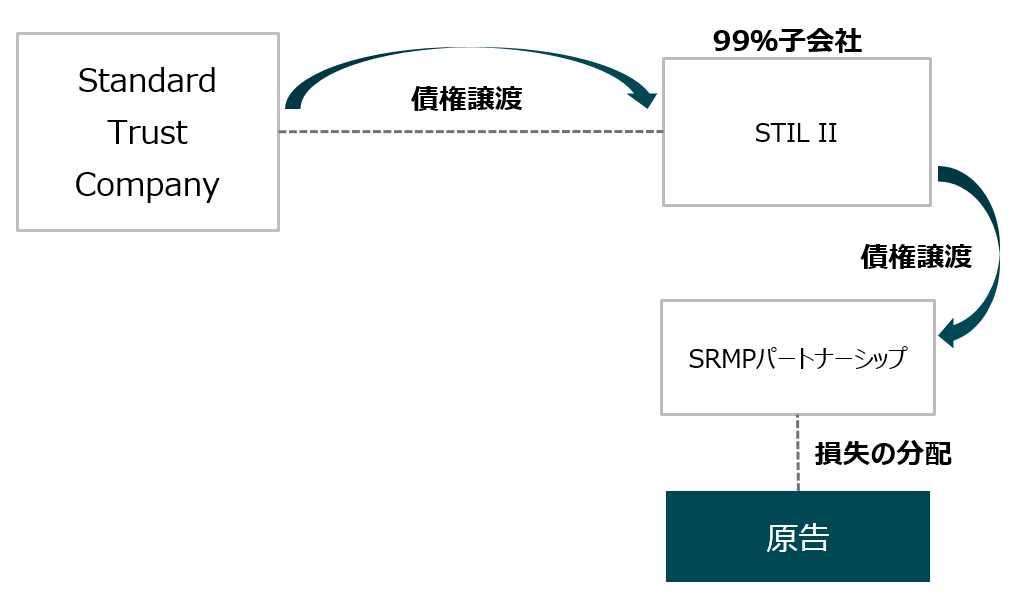

- ■概要

- ■Standard Trust Companyは不動産貸付けを行う会社であったが、1991年5月に破産して清算人が任命された。破産時には、Standard Trust Companyは9つの不動産で時価総額33,000,000カナダドルの不動産担保を持つ債権17件を有していた。この不動産の取得価格は85,000,000カナダドルで、Standard Trust Companyが清算すると役52,000,000カナダドルの損失が生じる状況であった。

■そこで以下の一連の取引が清算人によって考案された。

(1)Standard Trust Companyは全額出資の子会社STIL IIを設立する。

(2)Standard Trust Companyは含み損を持つ債権をSTIL IIに独立企業間価格ではない価格で譲渡する。

(3)STIL IIは、取得した債権を第三者であるSRMPパートナーシップに譲渡した。このSRMPパートナーシップの構成員の1人が原告である。STIL IIに起因する損失はSRMPの各メンバーに分配され、1993年および1993年10月期の所得計算において控除した上で申告を行った。

所得税法第18条第13項は、損失を関連者間で移転することにより通算させることを禁止している。従って、Standard Trust CompanyがSTIL IIを経由して第三者であるSRMPパートナーシップに損失を移転しても、当該損失を所得税法上他の所得と通算することはできない。しかし、STIL IIが第三者であるSRMPパートナーシップに当該損失を移転したのであれば、第18条に規定する制限の適用ななくなるため、SRMPパートナーシップが受領した損失は、SRMPパートナーシップをパススルーしてその構成員に帰属するというのが、納税者のプランであった。

■一審である租税裁判所、二審である控訴審ともに、納税者の主張を認めなかった。最高裁も、下級審の判断を支持し、国側を勝訴させた。

■最高裁は、Canada Trustco事案と同様、GAARの適用にあたり、以下の3つの基本的要素に言及した。

(1)租税上の便益が存在するか否か、(2)租税回避取引に該当するか否か、(3)租税法の濫用であるか否か。 - ■裁判所

- ■The Tax Court of Canada 2003(Taxpayer loses)(Appeal)

■The Federal Court of Appeal 2004 (Linden, Rothstein and Sexton JJ.A.)(Taxpayer loses)(Appeal)

■ Supreme Court of Canada October 19, 2005(McLachlin C.J. and Major J.)(Taxpayer loses)(Judgment Finalized)

争点

当該取引は租税回避取引に該当するか否か。

判決

■租税裁判所

→納税者敗訴

■控訴審

→納税者敗訴

■最高裁判所

→納税者敗訴

租税回避に対するカナダの動向

■現在のGAAR(General Anti-Avoidance Rule)は、所得税法だ第245条として導入された。その取扱い等については、カナダ歳入庁(Canada Revenue Agency: CRA)による通達がある。第245条h、カナダ所得税法(Income Tax Act)第16款の見出し「租税回避(Tax Avoidance)」に規定され、同条は前8項から構成される。同条第1項は、定義規定で有り、tax benefit(租税上の便益)、tax consequences(課税標準及び納税額等)、transaction(一連の取引を含む)が定義されている。

■GAARに対する評価と実績

GAARについてその取扱いを含む規定の内容の多くがカナダの納税義務者にとって不明瞭であったという評価がある。また、一般の税法の規定が技術的に正確な文言により規定されるのに対して、第245条自体が、不確定概念により定義されているため、曖昧であるとの指摘もある。カナダのGAARは、米国の最高裁判例のように、事業目的或いは経済的実質を導入しようとする立法意図であったが、英国のウエストミンスター貴族院判決(1935年)の影響が強いとの指摘もある。

■GAAR委員会の概要

GAAR委員会(the GAAR Committee)は、GAARの立法時にオタワに設置された。この委員会の役割は、税務調査により生じるGAARの適用可能性について審査することである。この委員会の構成員は、CRA、司法省、財務省の職員である。

■GAAR適用のプロセス

GAARの適用は次のようなプロセスで行われる。

①調査担当者がGAAR適用の可能性があるとして、濫用事案担当部門(the Aggressive Tax Planning Division)に上申し、同部門が調査を行う。

②調査担当者は、GAARの適用を分析して調査結果の書面(proposal letter)を納税義務者に送付し、納税義務者からの回答を待つ。納税義務者からの回答があると、調査担当者は担当部門にその内容と調査担当者の意見を添える。

③担当部門は、GAARの適用について。自らの調査と関連官庁との調整を行った上で、委員会に申請するか否かの最終判断をする。

④委員会の申請内容が新たな争点である場合には、担当部門が案を添え、そうでない場合は提言を行う。

⑤委員会は、GAARの適用に関する勧告を行う。

■GAARに関する主要な判例

GAARについての最高裁の判例は主に次の5事案が重要である。

①Stubart Investments Ltd. v. The Queen(1984)

②Canada Trustco Mortgage Co. v. Canada(2005)

③Mathew v. Canada(2005)

④Lipson v. Canada(2009)

⑤Copthorne Holdings Ltd. v. Canada(2011)

キーワード

■キーワード

GAAR (General Anti-Avoidance Rule)、Tax benefit、Abusive tax avoidance、Series of transactions、Income Tax Act、Partnership

■重要概念

一連の取引(Series of transactions)

両者の主張まとめ

納税者の主張

所得税法第18条第13項を適用し、未実現損失を第三者取引により移転したことで、損益通算が認められるべきである。

国税庁の主張

この取引は租税上の便益を得るための濫用型の租税忌回避取引(abusive tax avoidance)に該当する。所得税法上第245条第4項を適用し、納税者にパススルーされた損失の損益通算は認められない。

関連する条文

the Income Tax Act

Section 18(13) and Section 96(1)

Section 245(4)

Supreme Court of Canada October 19, 2005(McLachlin C.J. and Major J.)(Taxpayer loses)(Judgment Finalized)

OPINION

The purpose of s. 18(13) in particular is to prevent a taxpayer who is in the business of lending money from claiming a loss upon the superficial disposition of a mortgage or similar non-capital property. This purpose is achieved by confining the loss that would ordinarily be claimed by the transferor to a non-arm’s length transferee. Where s. 18(13) does not apply, only the transferor may claim the loss on the disposition, which would be consistent with the general policy of the Act against the transfer of losses.

Under s. 18(13), the loss is generally under the control of the transferor or traceable to the business of the transferor and is preserved because of its special relationship with the transferee partnership. The section in effect denies the loss to the transferor because it originated and remains in the transferor’s control before and after the transfer. To allow a new arm’s length partner to buy into the transferee partnership and thus to benefit from the loss would violate the fundamental premise underlying s. 18(13) that the loss is preserved because it essentially remains in the transferor’s control. It would contradict the main purpose of s. 18(13) and the premise on which it operates. Section 18(13) allows the preservation and transfer of a loss because of the non-arm’s length relationship between transferor and transferee. Absent that relationship, there is no reason for the provision to apply.

These observations suggest that the combined effect of s. 18(13) and the partnership provisions do not allow taxpayers to preserve and transfer unrealized losses to arm’s length parties. Section 18(13) relies on the premise that the partners in the transferee partnership pursue a business activity in common other than to transfer the loss and that the partnership and the transferor deal in a non-arm’s length relationship with respect to the property.

This brings us to the ultimate question of whether the only reasonable conclusion is that the series of transactions on which the appellants rely for the tax benefits they claim results in abusive tax avoidance when s. 18(13) and s. 96(1) are interpreted purposively, in the context of the Act as a whole.

As stated at para. 59 of Canada Trustco, a determination of whether there was abusive tax avoidance under s. 245(4) requires a close examination of the facts in order to determine whether allowing a tax benefit would be within the object, spirit or purpose of the provisions relied upon by the taxpayer. Although no single factual element is in itself determinative of whether there was abusive tax avoidance, the GAAR may be applied to deny a tax benefit “where the relationships and transactions as expressed in the relevant documentation lack a proper basis relative to the object, spirit or purpose of the provisions that are purported to confer the tax benefit, or where they are wholly dissimilar to the relationships or transactions that are contemplated by the provisions” (Canada Trustco, at para. 60).

We are of the view that to allow the appellants to claim the losses in the present appeal would defeat the purposes of s. 18(13) and the partnership provisions, and that the Minister properly denied the appellants the losses under the GAAR. Interpreted textually, contextually and purposively, s. 18(13) and s. 96 do not permit arm’s length parties to purchase the tax losses preserved by s. 18(13) and claim them as their own. The purpose of s. 18(13) is to transfer a loss to a non-arm’s length party in order to prevent a taxpayer who carries on a business of lending money from realizing a superficial loss. The purpose for the broad treatment of loss sharing between partners is to promote an organizational structure that allows partners to carry on a business in common, in a non-arm’s length relationship. Section 18(13) preserves and transfers a loss under the assumption that it will be realized by a taxpayer who does not deal at arm’s length with the transferor. Parliament could not have intended that the combined effect of the partnership rules and s. 18(13) would preserve and transfer a loss to be realized by a taxpayer who deals at arm’s length with the transferor. To use these provisions to preserve and sell an unrealized loss to an arm’s length party results in abusive tax avoidance under s. 245(4). Such transactions do not fall within the spirit and purpose of s. 18(13) and s. 96, properly construed.

The appellants’ submission that nothing in s. 18(13) limits subsequent dispositions of the property to arm’s length parties depends on a literal interpretation of the section and fails to address the main inquiry under the GAAR, which rests on a contextual and purposive interpretation of the provisions at issue. As discussed above, the text of the provision is open to a competing interpretation offered by the Minister and does not itself resolve the dispute. To do so, we must refer to the purposive construction of the provisions. The interplay of s. 18(13) and s. 96 requires us to look at the entire factual context of the series of transactions to determine whether it frustrates the object and spirit of these provisions.

The backdrop to the impugned transactions was the failure of STC, leaving non-performing mortgages in its wake. STC transferred $52 million in unrealized losses to Partnership A in a notionally non-arm’s length transaction. Partnership A was to serve as a holding tank for the unrealized losses and STC planned from the outset to sell its interest in Partnership A after the application of s. 18(13) so that the losses preserved in Partnership A could be transferred to arm’s length parties through a substitution of partners in Partnership A. The subsequent transactions involving Partnership B were executed “in contemplation of” the transactions between STC and Partnership A.

By these subsequent transactions, the losses preserved in Partnership A were transferred to Partnership B which sold units to the appellants, who dealt with STC at arm’s length. The new partnership, Partnership B, was relatively passive. From its inception, the purpose of Partnership B was simply to realize and allocate the tax losses, without any other significant partnership activity. Nor are these conclusions negated by the fact that (1) the underlying properties to the mortgages were appraised and sold or written off, (2) the appellants paid substantial amounts in order to acquire their interests in Partnership B, or (3) the appellants sought to minimize their exposure to risk, should the tax losses not be accepted by the authorities.

The abusive nature of the transactions is confirmed by the vacuity and artificiality of the non-arm’s length aspect of the initial relationship between Partnership A and STC. A purposive interpretation of the interplay between s. 18(13) and s. 96(1) indicates that they allow the preservation and sharing of losses on the basis of shared control of the assets in a common business activity. In this case, the absence of such a basis leads to an inference of abuse. Neither Partnership A nor Partnership B ever dealt with real property, apart from STC’s original mortgage portfolio. Nor was STC ever in a partnership relation with either OSFC or any of the appellants, having sold its entire interest to OSFC. The only reasonable conclusion is that the series of transactions frustrated Parliament’s purpose of confining the transfer of losses such as these to a non-arm’s length partnership.

As discussed in the companion case of Canada Trustco, where the Tax Court judge has applied the law correctly and made findings and inferences supported by the evidence, an appellate court should not interfere. Here the Tax Court judge, Dussault J.T.C.C., was obliged to apply the two-step approach mandated by the Federal Court of Appeal in OSFC. He was also obliged, at the first step, to accept the majority’s conclusion that the avoidance transactions at issue did not violate the spirit and purpose of s. 18(13). However, he went on to state at para. 304 that he preferred the minority view in OSFC that Parliament could not have intended for s. 18(13) to permit the transfer of losses between arm’s length taxpayers. In the result, had it been open to him, he would have applied the GAAR to disallow the losses on the basis of his interpretation of s. 18(13). We agree with these conclusions and endorse them.

Conclusion

We would dismiss the appeal with costs.

和訳

第 18 条(13)の目的は、特に、貸金業を営む納税者が、抵当権や類似の非資本財産の表面的な処分による損失を主張することを防止することである。 この目的は、通常であれば譲渡人が請求できる損失を、非対面譲渡人に限定することで達成される。 第 18 条(13)が適用されない場合、譲渡人のみが処分による損失を請求することができ、 これは損失の移転に対する法の一般的な方針と一致する。

18条13項では、損失は一般的に譲渡人の管理下にあるか、譲渡人の事業に追跡可能であり、譲受人のパートナーシップとの特別な関係により保全される。 同条項は、実質的に、損失が譲渡人の支配下にあり、譲渡の前後を問わず譲渡人の支配下にあるため、譲渡人の損失を否定するものである。 新たな独立企業間パートナーが譲受側のパートナーシップを買い取ることを認め、その結果、損失から利益を得ることを認めることは、損失は本質的に譲渡人の支配下にあるため維持されるという18条13項の基本的前提に反することになる。 これは、18条13項の主な目的とその前提に反することになる。 18条13項は、譲渡人と譲受人との間に非手先の関係があるからこそ、損失の保全と譲渡を認めているのである。 そのような関係がなければ、この規定が適用される理由はない。

以上の見解から、18 条 13 項とパートナーシップ規定の複合的な効果により、納税者が未実現損 失を保存し、独立企業間当事者に移転することはできないと考えられる。第 18 条(13)は、譲渡先のパートナーは、損失を譲渡すること以外に共通の事業活動を追求し、パートナ ーシップと譲渡人は、財産に関して独立企業間でない関係で取引していることを前提としている。

ここで、18 条(13)項と 96 条(1)項を法全体の文脈で合目的的に解釈した場合、控訴人らが主張する税制上の優遇措置の根拠 とする一連の取引が濫用的な租税回避につながるという結論だけが妥当であるかどうかという究極的な疑問が生じ る。

カナダ・トラストコのパラグラフ で述べられているように、租税回避の判断は、カナダ・トラストコ 5で述べられているように、245 条(4)に基づく濫用的な租税回避があったかどうかの判断は、租税優 遇を認めることが、納税者が依拠した規定の目的、精神、または目的の範囲内であるかどうかを判断 するために、事実を精査する必要があります。 濫用的な租税回避があったかどうかについては、単一の事実要素それ自体で決まるものでは ありませんが、GAAR は、「関連文書に表現されているような関係や取引が、租税優遇を与えるとされ ている規定の目的、精神、趣旨に照らして適切な根拠を欠く場合、または、規定が想定している関係や取 引とは全く異なる場合」に、租税優遇を否定するために適用される可能性があります(Canada Trustco, at para.60)。

我々は、本訴訟において控訴人らの損失請求を認めることは、18 条 13 項およびパートナーシップ規定の目的を逸脱するものであり、大臣は GAAR に基づき控訴人らの損失を適切に否認したとの見解を示す。 18条13項と96条は、条文的、文脈的、目的論的に解釈すると、18条13項によって保全される税務上の欠損金を購入し、それを自己のものとして主張することを、独立企業間当事者に認めているわけではない。 18条13項の目的は、貸金業を営む納税者が表面的な損失を被ることを防ぐために、損失を非関連当事者に移転することである。 パートナー間の損失分配を広く取り扱う目的は、非アームズレングスの関係において、パートナーが共同で事業を遂行できる組織構造を促進することにある。 第 18 条(13)は、譲渡人と独立企業間取引をしていない納税者が損失を実現することを前提に、損失を保全し、譲渡するものである。 パートナーシップ規定と第 18 条(13)項が相まって、譲渡人と独立の立場で取引する納税者が実現する損 失を保全し、譲渡することを国会が意図したとは考えられない。 これらの規定を利用して、未実現の損失を保全し、独立当事者へ売却することは、245 条(4)に基づく濫用的な租税回避となる。 このような取引は、適切に解釈される 18 条 13 項および 96 条の精神および目的には該当しない。

上訴人の主張は、第18条第13項には財産のその後の独立した当事者への譲渡を制限するものは何もないというものであり、これは条項の文字通りの解釈に依存しており、GAARの主要な調査事項である文脈的および目的的な解釈を無視している。前述のように、この条項の文言は大臣が提示する競合する解釈に開かれており、それ自体では紛争を解決しません。これを行うためには、条項の目的的な解釈に頼る必要がある。第18条第13項と第96条の相互作用は、一連の取引の全体的な事実関係を見て、これらの条項の目的と精神を損なうかどうかを判断する必要がある。

問題となっている取引の背景には、STCの失敗があり、これにより不良債権が残された。STCは、名目上の非独立取引でパートナーシップAに5200万ドルの未実現損失を移転しました。パートナーシップAは未実現損失の保管タンクとして機能し、STCは第18条第13項の適用後にパートナーシップAの持分を売却し、パートナーシップAに保存された損失をパートナーの交代を通じて独立した当事者に移転することを最初から計画していた。パートナーシップBに関わるその後の取引は、STCとパートナーシップAの間の取引を「考慮して」実行された。

これらの後続の取引により、パートナーシップAに保存された損失はパートナーシップBに移転され、パートナーシップBはSTCと独立して取引する上訴人にユニットを販売しました。新しいパートナーシップであるパートナーシップBは比較的受動的だった。パートナーシップBの目的は、設立当初から税損失を実現し配分することであり、他の重要なパートナーシップ活動はあらないだった。これらの結論は、(1)担保物件が評価され売却または償却されたこと、(2)上訴人がパートナーシップBの持分を取得するために多額の金額を支払ったこと、(3)税損失が当局に受け入れられない場合に備えてリスクを最小限に抑えようとしたことによっても否定されない。

Canada Trustcoの関連事件で議論されたように、税務裁判所の裁判官が法律を正しく適用し、証拠に基づいた発見と推論を行った場合、控訴裁判所は干渉すべきではない。ここで、税務裁判所の裁判官Dussault J.T.C.C.は、OSFCで連邦控訴裁判所が命じた二段階のアプローチを適用する義務があった。彼はまた、第一段階で、問題となっている回避取引が第18条第13項の精神と目的に違反していないという過半数の結論を受け入れる義務があった。しかし、彼はパラグラフ304で、議会が第18条第13項が独立した納税者間の損失の移転を許可することを意図していなかったというOSFCの少数意見を支持すると述べました。その結果、彼にその権限があった場合、彼は第18条第13項の解釈に基づいてGAARを適用し、損失を認めなかったろう。私たちはこれらの結論に同意し、支持する。

結論

上告を棄却する。

判示要旨

- 租税裁判所

- ■本事案の先例となる判決(OSFC Holdings Ltd v. Canada(2002))の判示を引用し、訴えを却下した。OSFCの事案判決は、2001年9月11日高裁判決、2002年6月20日に最高裁判決があり、いずれも国側の主張が認められたGAAR適用の事案である。

- 控訴裁判所

- ■本事案の事実関係が、OSFC事案判決と実質的に同様であり、OSFC事案判決に追随するものであるが、本判決は、GAARについて、2段階アプローチを採用した。すなわち、第1段階として、高裁は、所得税法第18条第13項と同法第96条の適用についてはこれを認めたが、第2段階として、租税法上の便益を認めることが、納税者間における損失を取引することを規制している所得税法の趣旨に反する、とのことから控訴人の請求は認められないとした。

- 最高裁判所

- ■上告人は、未実現損失を第三者取引により移転したことで、所得税法第18条第13項の適用を主張しているが、問題点は、パートナーシップが第三者に該当するか否かではなく、取引により生じるtax consequences(課税標準及び納税額等)が問題である。

■すなわち、所得税法上第245条第4項の適用の可否である。すなわち、この取引が租税上の便益を得るための濫用型の租税忌回避取引(abusive tax avoidance)に該当するか否かである。

■所得税法第18条第13項が適用となるパートナーシップの要件としては、第1に、金融業者が抵当権或いは類似する非有形固定資産を帆分し、第2に、パートナーシップが決められた期間の終了時に財産を取得する権利を有し、第3に、パートナーシップが当該納税義務者と独立企業間としいての取引をしていないことである。

■損失の控除を認めることは、所得税法第18条第13項とパートナーシップに係る規定の趣旨に反する。そのため、課税庁がGAARの規定を適用することを認める。本件において未実現の損失を第三者に譲渡することは、第245条第4項に規定する租税回避の濫用に該当する。

認定事実

FACTS

As a result of a series of transactions, the appellants lowered their incomes by deducting losses from the sale of mortgaged properties originally belonging to Standard Trust Company (“STC”). The overall arrangement involved three stages. At the first stage, STC transferred a portfolio of mortgages with unrealized losses to a non-arm’s length partnership, Partnership A, thereby acquiring a 99 percent interest in it. At the second stage, STC relied on s. 18(13) to transfer the unrealized losses to Partnership A and then sold its 99 percent interest in it to an arm’s length party. At the third stage, Partnership B was formed to acquire the 99 percent interest in Partnership A. The appellants joined Partnership B and were thus able to claim their proportionate shares of the losses from the eventual sale or write-down of the mortgaged properties. In this way, STC’s losses were transferred through s. 18(13) and the partnership vehicle to arm’s length taxpayers who offset them against their own incomes, while STC recovered a portion of the losses associated with the defaulted mortgages.

STC carried on a business which included the lending of money on the security of mortgages on real property. By May 1991, STC was insolvent and Ernst & Young was appointed as its liquidator. At that time, STC owned a portfolio of 17 non-performing loans with 9 underlying real estate properties having a fair market value of approximately $33 million, the “Portfolio Assets”. The cost to STC of the Portfolio Assets was approximately $85 million. Since STC was being liquidated, it could not use the approximately $52 million in unrealized losses from the Portfolio Assets.

The liquidator devised and oversaw the execution of a series of transactions to realize maximum returns on the disposal of the Portfolio Assets. The transactions are described in greater detail in a statement of admitted facts, which is reproduced at para. 5 of the decision of the Tax Court of Canada ([2003] 1 C.T.C. 2045). In sum, the appellants who are partners in a relatively passive partnership that dealt with STC at arm’s length deducted over $10 million of STC’s losses against their own incomes.

On October 21, 1992, STC incorporated a wholly owned subsidiary, 1004568 (the “subsidiary”). On October 23, 1992, STC and its subsidiary entered into a partnership agreement to create the STIL II Partnership (“Partnership A”). On that date, STC contributed the Portfolio Assets as capital for a 99 percent interest in Partnership A and the subsidiary borrowed $417,318 from STC to make its capital contribution for a 1 percent interest. At its inception, Partnership A did not deal with STC at arm’s length.

Section 18(13) of the Income Tax Act prohibits a taxpayer whose ordinary business includes the lending of money from deducting a loss on the disposition of a mortgage if at the end of a specified period, the mortgage is owned by a partnership that does not deal at arm’s length with the transferor. Under such circumstances, the loss is added to the cost of the mortgage to the partnership.

STC relied on s. 18(13) to transfer the Portfolio Assets into Partnership A at their historical cost of $85 million. From the outset, it was STC’s goal to use this transaction to preserve the unrealized losses of the Portfolio Assets of $52 million and to transfer them into Partnership A so that STC could eventually sell its 99 percent interest in Partnership A to an arm’s length party.

The partnership rules under s. 96 of the Act provide that a partnership’s income or losses flow through to its partners at the end of the taxation year. Partners are entitled to claim their proportionate shares of partnership losses, provided they are partners at the end of the taxation year, regardless of when they joined the partnership.

It was STC’s plan to sell its 99 percent interest in Partnership A to an arm’s length party so that Partnership A would dispose of the Portfolio Assets and realize losses of up to $52 million, and the new partner would rely on s. 96 of the Act to claim 99 percent of the losses. Between August 1992 and January 1993, STC contacted 38 prospective purchasers for its 99 percent interest in Partnership A.

In January 1993, STC began negotiations with OSFC Holdings Ltd. (“OSFC”), an arm’s length corporation. On May 31, 1993, STC and OSFC agreed on the purchase and sale of the 99 percent interest in Partnership A. One of the terms of the purchase agreement was that OSFC would pay to STC an adjustable “Additional Payment” of up to $5 million if Partnership A realized losses from the disposition of the Portfolio Assets for income tax purposes. The result of this term was to convert STC’s $52 million in unrealized losses into up to $5 million in cash for STC.

By September 30, 1993, as a result of the sale of some of the Portfolio Assets and the write-down of the remaining assets to fair market value, Partnership A realized losses in excess of $52 million. Partnership A allocated 99 percent of its losses to Partnership B which then allocated these losses to its partners, including the appellants.

The appellants together deducted over $10 million of the Partnership B losses against their own incomes in 1993 or 1994. Some of the appellants, in addition to reducing their taxable incomes for the relevant year to NIL, also computed non-capital losses to be carried forward or back.

The Minister of National Revenue reassessed the appellants, applied the GAAR, and disallowed the deduction of their share of the Partnership B losses.

和訳

一連の取引の結果、上訴人は、元々Standard Trust Company(「STC」)に属していた抵当物件の売却による損失を控除することで所得を減少させた。

全体の取り決めは三段階に分かれていた。第一段階では、STCは未実現損失を伴う抵当ポートフォリオを非独立のパートナーシップであるパートナーシップAに移転し、99%の持分を取得した。

第二段階では、STCは第18条第13項に基づいて未実現損失をパートナーシップAに移転し、その後、99%の持分を独立した当事者に売却した。

第三段階では、パートナーシップBが設立され、パートナーシップAの99%の持分を取得した。

上訴人はパートナーシップBに参加し、抵当物件の最終的な売却または評価減による損失の割合を請求することができた。このようにして、STCの損失は第18条第13項およびパートナーシップの仕組みを通じて独立した納税者に移転され、彼らは自分の所得に対してこれらの損失を相殺し、STCは不良債権に関連する損失の一部を回収した。

STCは、不動産の抵当を担保にした貸付業務を含む事業を行っていた。1991年5月までにSTCは破産し、Ernst & Youngが清算人として任命された。

その時点で、STCは17件の不良債権を含むポートフォリオを所有しており、そのうち9件の不動産の公正市場価値は約3300万ドルだった(「ポートフォリオ資産」)。STCのポートフォリオ資産のコストは約8500万ドルだった。STCが清算されていたため、ポートフォリオ資産からの約5200万ドルの未実現損失を利用することはできなかった。

清算人は、ポートフォリオ資産の処分で最大のリターンを実現するための一連の取引を考案し、実行を監督しました。これらの取引は、カナダ税務裁判所の決定([2003] 1 C.T.C. 2045)のパラグラフ5に再現された事実の認定書に詳述されている。要するに、STCと独立して取引する比較的受動的なパートナーシップのパートナーである上訴人は、STCの損失のうち1000万ドル以上を自分の所得に対して控除した。

1992年10月21日、STCは完全子会社である1004568(「子会社」)を設立しました。1992年10月23日、STCとその子会社はパートナーシップ契約を締結し、STIL IIパートナーシップ(「パートナーシップA」)を設立しました。その日に、STCはパートナーシップAの99%の持分としてポートフォリオ資産を資本として提供し、子会社はSTCから417,318ドルを借りて1%の持分のための資本を提供しました。設立当初、パートナーシップAはSTCと独立して取引していなかった。

所得税法第18条第13項は、通常の事業において金銭の貸付を行う納税者が、指定された期間の終わりにおいて譲渡者と独立して取引しないパートナーシップが抵当を所有している場合、抵当の処分による損失を控除することを禁止している。こじみた状況では、損失はパートナーシップの抵当のコストに加算される。

STCは、第18条第13項に基づいてポートフォリオ資産を歴史的コストの8500万ドルでパートナーシップAに移転しました。最初から、STCの目標は、この取引を利用してポートフォリオ資産の未実現損失5200万ドルを保存し、それをパートナーシップAに移転することだった。

法の第96条に基づくパートナーシップ規則は、パートナーシップの収入または損失が課税年度の終わりにパートナーに流れることを規定している。パートナーは、課税年度の終わりにパートナーである限り、パートナーシップの損失の割合を請求する権利がある。

STCの計画は、パートナーシップAの99%の持分を独立した当事者に売却し、パートナーシップAがポートフォリオ資産を処分して最大5200万ドルの損失を実現し、新しいパートナーが法の第96条に基づいて損失の99%を請求することだった。1992年8月から1993年1月の間に、STCはパートナーシップAの99%の持分のために38人の見込み購入者に連絡した。

1993年1月、STCは独立した法人であるOSFC Holdings Ltd.(「OSFC」)との交渉を開始しました。1993年5月31日、STCとOSFCはパートナーシップAの99%の持分の購入および売却に合意しました。購入契約の条件の一つは、パートナーシップAが所得税目的でポートフォリオ資産の処分から損失を実現した場合、OSFCがSTCに最大500万ドルの調整可能な「追加支払い」を行うことだった。この条件の結果、STCの5200万ドルの未実現損失は、STCに最大500万ドルの現金に変換された。

1993年9月30日までに、ポートフォリオ資産の一部の売却および残りの資産の公正市場価値への評価減の結果、パートナーシップAは5200万ドルを超える損失を実現しました。パートナーシップAは損失の99%をパートナーシップBに配分し、パートナーシップBはこれらの損失を上訴人を含むパートナーに配分した。

上訴人は1993年または1994年にパートナーシップBの損失のうち1000万ドル以上を自分の所得に対して控除しました。一部の上訴人は、該当年の課税所得をゼロに減少させるだけでなく、繰越または繰戻し可能な非資本損失も計算した。

国税庁長官は上告人を再査定し、GAARを適用してパートナーシップBの損失の控除を認めなかった。

(補足)Mathew事案とは

GAARの適用を巡る重要判例

■Mathew v. Canada, [2005] は、カナダ最高裁判所が決定した重要な事件で、所得税法における一般的な反回避規則(GAAR)の適用に関するものである。

■背景

この事件は、破産状態にあったStandard Trust Company(STC)に関するもので、STCは多額の未実現損失を伴う不良債権のポートフォリオを保有していた。

STCはこれらの損失をパートナーシップ(パートナーシップA)に移転し、その後、パートナーシップの持分を独立した当事者に売却しました。この一連の取引により、新しいパートナーである上訴人は、自分の所得に対してこれらの損失を請求することができた。

■法的問題

主な法的問題は、この一連の取引がGAARの下で濫用的な税回避に該当するかどうかだった。

GAARの適用には、税の利益、回避取引、および所得税法の条項の誤用または濫用の3つの要素が必要である。

裁判所の分析:

裁判所は、取引が税の利益を得る以外の正当な目的で行われたかどうかを検討した。

また、取引が所得税法の特定の条項を誤用したか、または法全体を濫用したかどうかも考慮しました1。

判決:

最高裁判所はGAARの適用を支持し、取引が主に税の利益を得ることを目的としており、濫用的な税回避に該当すると結論付けた。

裁判所は、税法の条項を解釈する際には、統一された文言、文脈、および目的に基づくアプローチの重要性を強調した。

■影響

この事件は、Canada Trustco Mortgage Co. v. Canadaとともに、カナダの税法におけるGAARの適用に関する重要な先例判決となった。

経済的実質のない取引を通じて得られた税の利益がGAARの下で否定される可能性があるという原則を強化したのである。

編集者コメント

GAARの適用を巡る攻防 Mathew v. Canada, [2005]の意義

■Mathew v. Canada, [2005]**は、カナダ最高裁判所がGAAR(一般的な反回避規則)の適用に関して重要な判断を下した事案である。この事件は、破産状態にあったStandard Trust Company(STC)が多額の未実現損失を伴う不良債権のポートフォリオを保有していたことに端を発する。STCはこれらの損失をパートナーシップAに移転し、その後、パートナーシップの持分を独立した当事者に売却しました。この一連の取引により、新しいパートナーである上訴人は、自分の所得に対してこれらの損失を請求することができた。

■最高裁判所は、GAARの適用には三つの要素が必要であるとした。(1)租税上の便益が存在するか否か、(2)租税回避取引に該当するか否か、(3)租税法の濫用であるか否か、である。

■裁判所は、取引が税の利益を得る以外の正当な目的で行われたかどうかを検討し、また、取引が所得税法の特定の条項を誤用したか、または法全体を濫用したかどうかを考慮した。最終的に、最高裁判所はGAARの適用を支持し、取引が主に税の利益を得ることを目的としており、濫用的な税回避に該当すると結論付けた。

■この判決は、Canada Trustco Mortgage Co. v. Canadaとともに、カナダの税法におけるGAARの適用に関する重要な先例となっている。経済的実質のない取引を通じて得られた税の利益がGAARの下で否定される可能性があるという原則を強化し、将来の税回避事案に対する裁判所のアプローチに大きな影響を与えるものとなった。

重要概念/一連の取引(Series of transactions)

租税回避における『一連の取引』の概念とその法的意義

■「一連の取引」という概念は、租税回避の分野において極めて重要な役割を果たする。これは、複数の取引が連続して行われ、その全体が一つの目的、特に税の利益を得るために設計されている場合に適用される。

■「一連の取引」とは、個々の取引が独立して存在するのではなく、全体として一つの目的を達成するために計画され、実行される取引の集合体を指す。この概念は、税法の適用において、特にGAAR(一般的な反回避規則)の文脈で重要である。GAARは、租税回避を防止するための規則であり、納税者が税の利益を得るために行う取引が、法の趣旨や目的に反する場合に適用される。

■一般に、一連の取引が存在するかどうかを判断するためには、以下の要素が考慮される。

取引の連続性:取引が時間的に連続して行われているかどうか。

取引の関連性:各取引が相互に関連し、全体として一つの目的を達成するために設計されているかどうか。

目的の一貫性:取引全体が一つの主要な目的、特に税の利益を得るために行われているかどうか。

■法的適用と判例

カナダの最高裁判所は、Mathew v. Canada, [2005]において、「一連の取引」の概念を詳細に検討した。この事件では、Standard Trust Company(STC)が未実現損失をパートナーシップに移転し、その後、独立した当事者に売却する一連の取引が問題となった。裁判所は、これらの取引が全体として税の利益を得るために設計されており、GAARの適用対象となると判断したのである。

■「一連の取引」という概念は、租税回避を防止するための重要な考え方である。これにより、納税者が複数の取引を通じて租税法の便益を得ようとする場合でも、その全体が法の趣旨や目的に反する場合には、税の利益が否定される可能性がある。

併せて読みたい/カナダ・トラスト事案

Canada Trustco Mortgage Co. v. Canada

■最高裁判所2005年10月19日判決の事案である。Mathew事案と同年同日の判決であるが、本判決はGAARの適用を認めず、Mathew事案最高裁判決はGAARの適用を認めるという内容から、対比されるものである。

■カナダ・トラスト社(Canada Trustco Mortgage Co.)は、金融会社である。同社は、1996年12月17にちに多くのトレイラー車を1億2千万カナダドルでリース会社(Transamerical Leasing Inc.)から購入し、これらを同日に有限責任会社である英国法人(Maple Assets Investment Limited)にリースした。その目的は、1997課税年度において、トレイラー車の税務上の減価償却を請求することであった。

■Maple Assets Investment Limitedからransamerical Leasing Inc.に、再リースが行われた。トレイラー車の購入資金は、ジャージーの信託銀行(Rotal Band of Canada Trust Company Limited)からノンリコースで借入れをした。その後、Canada Trustco Mortgage Co.はMaple Assets Investment Limitedから受け取る債権を信託銀行に譲渡した。

■課税庁が、Canada Trustco Mortgage Co.の減価償却を否認したことから、Canada Trustco Mortgage Co.が訴えを起こした事件である。

■一審である租税裁判所h、所得税法に規定うる減価償却に係る趣旨と目的に合致しているとして、納税者の主張を認めた。控訴審も、一審を支持し、GAARの適用は出来ないとした。最高裁も、下級審の判断を支持し、課税庁の主張を斥けた。